Introduction

Healthcare costs are projected to average $18,500 per employee in 2026—a 6.7% increase from the prior year. Talent retention pressures are pushing more organizations toward comprehensive wellness programs. What many HR leaders don't realize: the IRS rewards these investments with measurable tax advantages.

Wellness programs are frequently discussed in terms of culture and engagement. Their real financial value, though, shows up on the balance sheet — through lower payroll taxes, deductible program costs, and higher employee take-home pay. This article breaks down how employer-sponsored wellness programs create tax benefits for both sides, what qualifies under IRS rules, and how to structure programs to capture those savings.

Key Takeaways

- Employers deduct wellness program costs as ordinary business expenses, reducing taxable income

- Section 125 cafeteria plans let employees pay wellness expenses pre-tax, cutting employer FICA payroll tax obligations in the process

- Employees reduce their own taxable income and payroll taxes by contributing pre-tax dollars to qualified wellness expenses

- Cash rewards and reimbursements of pre-taxed contributions are generally taxable under IRS rules

- Higher enrollment multiplies savings — a 100-person workforce on a Section 125 plan can save an employer thousands in annual FICA costs alone

What Are Employer-Sponsored Wellness Programs?

Employer-sponsored wellness programs are structured workplace initiatives that promote physical, mental, and financial health. These programs include fitness benefits, health screenings, smoking cessation support, stress management resources, nutrition counseling, and Employee Assistance Program (EAP) services.

These programs sit at the intersection of employee benefits strategy and tax planning. When properly structured, they function as a tax-advantaged compensation tool with real financial upside for both employer and employee. The IRS provides defined pathways for both sides to realize those benefits, making wellness programs one of the few HR initiatives that can reduce net compensation costs while improving workforce health.

Tax Benefits for Employers

Employers can access wellness-related tax benefits through two primary mechanisms: direct business expense deductions and payroll tax savings from pre-tax benefit structures.

Deducting Wellness Program Costs as Business Expenses

Under IRS rules, costs incurred to establish and run a wellness program are generally deductible as ordinary and necessary business expenses under IRC Section 162. This includes:

- Vendor fees for wellness platforms and services

- Wellness coordinator salaries

- Health screening and biometric testing costs

- Educational materials and resources

- Wellness technology and software subscriptions

Deducting these costs reduces the employer's net taxable income—meaning the government effectively subsidizes a portion of the program investment. At the 21% federal corporate tax rate, every $100,000 in deductible wellness expenses yields $21,000 in federal income tax offsets.

Comprehensive wellness programs typically range from $150 to $1,200 per employee annually, depending on the inclusion of coaching, biometrics, and incentives. For an organization with 500 employees spending $700 per employee on a comprehensive program ($350,000 total), the federal tax deduction value at 21% equals $73,500—significantly reducing the net program cost.

Companies with larger employee populations and more comprehensive programs see proportionally larger deductions, making this advantage especially meaningful at scale.

Payroll Tax Savings Through Section 125 Cafeteria Plans

Section 125 cafeteria plans allow employees to pay for eligible wellness benefits using pre-tax payroll deductions, which the IRS treats as employer contributions. This reduces the taxable wage base for both employee and employer.

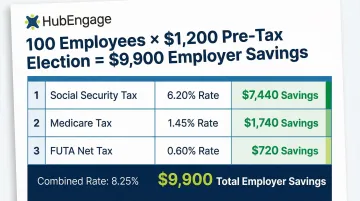

For every dollar an employee elects toward eligible wellness expenses pre-tax, the employer avoids paying FICA (Social Security and Medicare) and FUTA taxes on that amount.

Concrete example: Consider 100 employees who each elect $1,200 annually in pre-tax wellness benefits through a Section 125 plan ($120,000 total):

| Tax Category | 2026 Employer Rate | Employer Savings |

|---|---|---|

| Social Security (OASDI) | 6.20% | $7,440 |

| Medicare | 1.45% | $1,740 |

| FUTA (net after credit) | 0.60% | $720 |

| Total Payroll Tax Savings | 8.25% | $9,900 |

This immediate, guaranteed payroll tax savings effectively subsidizes the administrative costs of the wellness program. Organizations with larger workforces or higher participation rates see proportionally larger savings—the benefit scales directly with headcount and employee election amounts.

Tax Benefits for Employees

Employees benefit in two ways: lower taxable income through pre-tax elections, and access to certain wellness benefits that qualify as non-taxable fringe benefits.

Pre-Tax Contributions and Reduced Taxable Income

When employees elect to participate in a Section 125 wellness plan, their contributions are deducted before federal income tax, state income tax (in most states), and FICA. This reduces their overall taxable wage and increases effective take-home pay without a raise.

Practical example: Consider an employee in the 22% federal tax bracket who contributes $1,200 annually to wellness benefits pre-tax:

- Federal income tax savings: $264 ($1,200 × 22%)

- FICA tax savings: $91.80 ($1,200 × 7.65%)

- Total annual tax savings: $355.80

For a single filer in the 12% bracket, the same $1,200 election saves $235.80 annually. For a married couple filing jointly in the 24% bracket, savings reach $379.80.

Pre-tax access makes wellness services more affordable, which drives participation — and higher participation generates employer tax savings in return. Both sides benefit from the same election.

Tax-Free Fringe Benefits for Employees

Certain wellness benefits qualify as excludable fringe benefits under IRC Section 132, meaning employees receive them without recognizing taxable income. Examples include:

- On-site fitness facilities operated by the employer

- Qualifying on-site health services

- De minimis items like wellness merchandise or t-shirts

One critical rule: The benefit must be a legitimate qualifying service or item — not a cash equivalent or reimbursement of an already pre-taxed expense. Many programs get this wrong by offering cash incentives or gift cards, which are always taxable regardless of how they're framed.

Structured correctly, these benefits increase employee compensation value without increasing payroll costs — a straightforward win for both HR leaders and the workforce they support.

What Qualifies (and What Doesn't) for Tax-Advantaged Treatment

The IRS has issued specific guidance on this — IRS Memorandum 201622031 and Chief Counsel Advice 202323006 both clarify that not all wellness incentives receive favorable tax treatment. Getting the distinction wrong means unexpected payroll tax liability — for both the employer and the employee.

Eligible for Tax-Favorable Treatment

The following categories typically qualify for tax-advantaged treatment:

- Preventive screenings and health assessments — Employer-paid biometric screenings, blood pressure checks, and health risk assessments

- Smoking cessation programs — These qualify as medical care because they treat tobacco use disorder

- Nutrition and weight management counseling — When prescribed by a physician to treat a specific disease like obesity or hypertension

- Mental health EAP services — Counseling, stress management, and behavioral health support

- Medical care under IRC Section 213(d) — Services that diagnose, cure, mitigate, treat, or prevent disease

- HSA contributions — Employer contributions to employee Health Savings Accounts paired with high-deductible health plans (HDHPs)

On HSA contributions: Employer HSA contributions are deductible for the employer and excluded from the employee's gross income — giving both sides a tax benefit in one move. For 2026, contribution limits are $4,400 for self-only coverage and $8,750 for family coverage.

What Generally Does NOT Qualify

Several common program structures fall outside tax-favorable treatment:

- Cash rewards and gift cards — Payments for completing wellness activities are not excludable from gross income and must be included in wages subject to FICA/FUTA withholding, regardless of how the program is framed

- Double-dipping on pre-tax premiums — Employers cannot reimburse premiums already excluded through a cafeteria plan election; IRS Revenue Ruling 2002-3 treats this as taxable income to the employee

- Fixed-indemnity wellness payments — IRS CCA 202323006 clarified that lump-sum payments from plans funded by pre-tax premiums are taxable wages when the employee has no actual out-of-pocket medical costs (for example, a $1,000 health screening payment is fully taxable if no medical expenses were incurred)

Quick Reference: Qualifies vs. Does Not Qualify

| Qualifies for Tax-Favorable Treatment | Does NOT Qualify (Taxable to Employee) |

|---|---|

| Preventive health screenings | Cash rewards for participation |

| Smoking cessation programs | Gift cards and cash equivalents |

| Physician-prescribed weight loss | Gym membership reimbursements |

| Mental health counseling | Reimbursement of pre-tax premiums |

| On-site fitness facilities | Fixed-indemnity wellness payments |

| Employer HSA contributions | General wellness merchandise of significant value |

How to Maximize Your Wellness Program Tax Benefits

The tax value of a wellness program scales directly with participation. The more employees who enroll and elect benefits, the greater the payroll tax savings for both sides. This makes employee awareness and adoption a financial imperative, not just an engagement goal.

Structural Requirements for IRS Compliance

Employers must meet specific requirements to maintain IRS compliance:

- Written plan document — Section 125 cafeteria plans must be documented in a separate written plan maintained by the employer

- Nondiscrimination testing — Benefits must be available to all similarly situated employees, not just highly compensated individuals

- Proper recordkeeping — Maintain detailed records of program expenses, employee elections, and benefit distributions

- Coordination with benefits specialists — Work with qualified payroll and benefits professionals for Section 125 administration

- FSA contribution limits — For 2026, health FSA salary reduction contributions must be capped at $3,400; exceeding this limit disqualifies the entire cafeteria plan

Driving Participation Through Communication

Consistent, multi-channel communication is essential. Average wellness program participation rates hover around 30-35%, leaving significant tax savings unrealized. Employees who don't know about the program—or don't understand the pre-tax value—won't enroll.

The gap is most pronounced among frontline and deskless workers, who contend with:

- No regular access to company intranets or desktops during shifts

- Irregular schedules that make synchronous communications easy to miss

- Physical fatigue that reduces engagement with non-essential information

Research shows that digital nudges—such as text messages and app alerts—are effective at increasing exercise participation within corporate wellness programs. Platforms like HubEngage are built for exactly this challenge, using mobile apps, SMS, email, and digital signage to reach distributed teams across every shift and location. Its gamification features—points, badges, and leaderboards—give employees a concrete reason to engage, which translates directly into higher enrollment and greater tax savings for the organization.

Regular Audits and Professional Consultation

HR teams should regularly audit wellness program expenses and consult a tax professional annually to ensure continued compliance and to capture any new IRS guidance or legislative changes. Tax law evolves, and what qualified last year may have new restrictions or opportunities this year.

Frequently Asked Questions

Are employee wellness program expenses tax deductible?

Yes, employers can generally deduct wellness program costs as ordinary business expenses under IRC Section 162, reducing taxable income. Employees can exclude certain wellness benefits from their taxable wages when programs are structured through a Section 125 cafeteria plan.

How does the new $6,000 tax deduction work?

The $6,000 deduction refers to a temporary enhanced tax deduction specifically for seniors (individuals age 65 and older) for tax years 2025 through 2028, created by the "One Big Beautiful Bill Act." It has no connection to employer-sponsored wellness programs, FSAs, or HSAs.

What qualifies as a tax-free wellness benefit under IRS rules?

Benefits qualifying as medical care under IRC Section 213(d)—such as preventive screenings, smoking cessation, nutrition counseling prescribed for specific diseases, and mental health services—receive tax-favorable treatment. Cash rewards and non-medical perks typically do not qualify.

Are cash rewards from wellness programs considered taxable income?

Yes, per IRS Memorandum 201622031, cash rewards paid for wellness program participation are taxable wages subject to income tax and FICA withholding. They cannot be excluded even when the employer structures the program as a Section 125 cafeteria plan.

What is a Section 125 cafeteria plan and how does it apply to wellness programs?

A Section 125 cafeteria plan is an IRS-approved framework that allows employees to pay for eligible benefits with pre-tax dollars, lowering taxable income for employees and payroll tax costs for employers. Wellness programs structured under this framework qualify employees to make pre-tax contributions toward eligible benefits.

Can small businesses take advantage of wellness program tax benefits?

Yes, businesses of any size can implement Section 125-compliant wellness programs and claim business expense deductions. The savings scale with workforce size, but even small employers benefit from reduced FICA obligations and lower overall payroll tax liability.